Brad Setser's post today regarding "Why is China’s government trying so hard to hold down China’s current living standard?" is an excellent discussion of the issues facing China's leaders today. Here is a response that I posted at his blog:

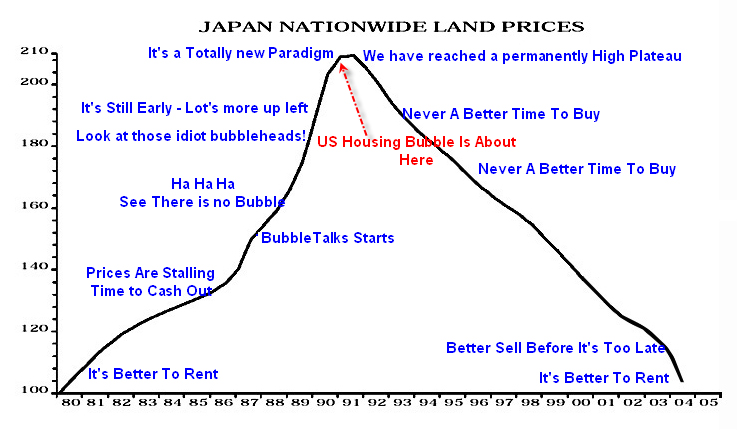

This description of China today sounds an awful lot like descriptions of Japan in 1989 when Japan's economic boom was at its peak. If one substitutes "Japan" for "China" in your statement "China’s government has had a policy of, in effect, subsidizing the use of Chinese labor for the production of goods for export" you would have a fair description of Japanese domestic labor policy. At that time, Japan's export sector was being subsidized at the expense of Japanese consumers, who in spite of the massive increase in GDP that had taken place since the 1970's who had a lower average standard of living than US consumers. As an example, one could purchase Japanese-made cameras more cheaply in the US than in the markets at Akihabara in Tokyo. Japanese people lived in tiny apartments or homes (and still do) compared to their US counterparts. Japanese companies paid huge amounts for US assets, particularly real estate, that turned out to have been gross overpayments (think of the Pebble Beach golf course).

I think that the core issue for the PBoC is that if the RMB is allowed to go to its market price, then China's export sector will suffer severely. Given that the export sector has been the primary source of per capita income improvement, the PBoC is reluctant to kill this golden goose, even though it knows that RMB appreciation is needed in the long run.

Also, if China allows wages to increase, that would funnel through to increased prices for Chinese goods on the world market leading to some amount of negative export growth. The key is to balance the increase in domestic consumption that would result from higher wages with the decrease in exports. I don't think that it is humanly possible to manage that balance without dislocations. When the dislocations come, Chinese leaders can point fingers at the US all day long, but the talk won't mean anything. Especially when Chinese policy has been to systematically torpedo US investment in tradables production capacity.

To get back to my analogy with Japan, I would say that China can now look forward to a similar long period of stagnation in sectors that have been experiencing bubble-like growth and difficulty in getting GDP growth from the domestic sector.

Wednesday, February 28, 2007

Links of the day

Nikkei 225 Falls Nearly 3% on Broad Selling....the main point from this post is the following nugget: "Japan's industrial production in January was its biggest month-over-month drop in three years, meaning there really seems to be no reason for a follow-on near-term Bank of Japan rate hike."...in my view, even though Japanese carmakers are taking market share from Detroit, US demand for cars has to be moderating because of all the vehicles that have been bought in the last three to five years...consumers are going to be in the mode of milking their current vehicles rather than buying a new one...

Bullish On The Yen Following The Selloff...gives good background on yen fundamentals and the mechanics of the

carry trade...

Investing In Taiwan...good background on this country...

Bullish On The Yen Following The Selloff...gives good background on yen fundamentals and the mechanics of the

carry trade...

Investing In Taiwan...good background on this country...

Tuesday, February 27, 2007

Hilarious statement of the day

From an excellent post by Richard Benson at PrudentBear.com titled "Subprime Titanic Hits Iceberg: Wall Street Abandons Ship" comes this statement:

Benson elaborates on the reality of this business:

No kidding....

"The securitization mortgage business relies on trusting the mortgage brokers and bankers, who make representations on aspects of loans and borrower quality."

Bwahahaha......that's enough to make me roll on the floor with laughter.Benson elaborates on the reality of this business:

The subprime market is overloaded with bad loans that have effectively smashed holes into the hull of this financial ship. It has been surprisingly easy for people buying a new house to borrow hundreds of thousands of dollars by simply telling the bank how much money they make -- without any proof. It's called a "stated income" loan, but many people inside the housing industry call it something else: a “liar loan” or a “NINA” (no asset, no income verification). Forty percent of the subprime market (about $400 - $500 billion of loans), is made up of these loans. At best estimates, half of all subprime mortgages had no income verification. This is no small problem!

No kidding....

Greenspan helps out his pal Bernanke

The media is pointing to comments Alan Greenspan made recently as a factor in today's market drops. The AP says that

"Investors were also spooked by comments Monday from former Federal Reserve Chairman Alan Greenspan, who said a recession in the U.S. was "possible" later this year."

Also, "In comments to a business conference in Hong Kong on Monday, Greenspan said the U.S. economy has been expanding since 2001 and that there are signs the current economic cycle is coming to an end."When you get this far away from a recession, invariably forces build up for the next recession, and indeed we are beginning to see that sign," Greenspan said. "For example in the U.S., profit margins ... have begun to stabilize, which is an early sign we are in the later stages of a cycle.""While, yes, it is possible we can get a recession in the latter months of 2007, most forecasters are not making that judgment and indeed are projecting forward into 2008 ... with some slowdown," he said."

Greenspan can say this without repercussion since he is retired; he's helping Bernanke out by stating the facts where Bernanke couldn't say the same thing without serious repercussions.

"Investors were also spooked by comments Monday from former Federal Reserve Chairman Alan Greenspan, who said a recession in the U.S. was "possible" later this year."

Also, "In comments to a business conference in Hong Kong on Monday, Greenspan said the U.S. economy has been expanding since 2001 and that there are signs the current economic cycle is coming to an end."When you get this far away from a recession, invariably forces build up for the next recession, and indeed we are beginning to see that sign," Greenspan said. "For example in the U.S., profit margins ... have begun to stabilize, which is an early sign we are in the later stages of a cycle.""While, yes, it is possible we can get a recession in the latter months of 2007, most forecasters are not making that judgment and indeed are projecting forward into 2008 ... with some slowdown," he said."

Greenspan can say this without repercussion since he is retired; he's helping Bernanke out by stating the facts where Bernanke couldn't say the same thing without serious repercussions.

Links of the day

The Portable Alpha Trade-off: Beta Leverage for Alpha Diversification...Good explanation of the concepts of portable alpha

Debt-market bomb could hurt us all...excellent analysis of derivatives and their effects

Will Hong Kong Shanghai Bank Be the New Credit Anstalt....from PrudentBear.com...thought-provoking analogy with a bank that collapsed at the end of the Weimar era in Germany...I added Prudent Bear to my links as it is an excellent site...

Intel Adds Insult To Injury With Latest Production Investment...a contrarian view on Intel's investment in 45 nm production facility...

Debt-market bomb could hurt us all...excellent analysis of derivatives and their effects

Will Hong Kong Shanghai Bank Be the New Credit Anstalt....from PrudentBear.com...thought-provoking analogy with a bank that collapsed at the end of the Weimar era in Germany...I added Prudent Bear to my links as it is an excellent site...

Intel Adds Insult To Injury With Latest Production Investment...a contrarian view on Intel's investment in 45 nm production facility...

Credit standards tightening beyond subprime

Nouriel Roubini's Blog has kindly posted a piece by Richard Berner of Morgan Stanley titled "Credit Crunch Watch". Some of the key points from the post:

-"Fed data indicate that delinquencies on non-mortgage consumer loans at commercial banks have risen about 15 bp from their record lows at the end of 2005; most of this is traceable to a rise in credit-card delinquencies of about 60 bp to 4.11% over the same period. S&P data for securitized card portfolios show virtually identical results. This is hardly surprising, given the “adverse selection” in cards resulting from better-quality borrowers switching from credit card into mortgage credit over the past several years."

-"Banks aren’t the primary originators of subprime loans, but the deterioration in subprime mortgage credit quality may have already triggered sharply tighter bank lending standards to individuals, judging by the Fed’s January Senior Loan Officer survey. Sixteen percent of responding banks on net reported tightening lending standards for residential mortgages — the biggest surge since 1990." ---The biggest surge since 1990 sounds like a significant tightening to me.

-"Lenders, understandably against that backdrop, have stopped loosening their lending standards to corporate borrowers, according to the Fed’s Senior Loan Officer Survey."

-(Morgan Stanley) "is expecting chargeoffs to remain flat this year, but loan provisions to rise 30% as falling recoveries spell the end to the long improvement in credit quality."---Has the equity market priced in the expectation of increasing reserves?

-"Even a slight reduction in market liquidity will make it more difficult efficiently to lay off risk, so lending standards will likely tighten further."---That seems like a reasonable statement to me.

There is are a number of other points to chew on in Roubini's post; it's well worth a read.

-"Fed data indicate that delinquencies on non-mortgage consumer loans at commercial banks have risen about 15 bp from their record lows at the end of 2005; most of this is traceable to a rise in credit-card delinquencies of about 60 bp to 4.11% over the same period. S&P data for securitized card portfolios show virtually identical results. This is hardly surprising, given the “adverse selection” in cards resulting from better-quality borrowers switching from credit card into mortgage credit over the past several years."

-"Banks aren’t the primary originators of subprime loans, but the deterioration in subprime mortgage credit quality may have already triggered sharply tighter bank lending standards to individuals, judging by the Fed’s January Senior Loan Officer survey. Sixteen percent of responding banks on net reported tightening lending standards for residential mortgages — the biggest surge since 1990." ---The biggest surge since 1990 sounds like a significant tightening to me.

-"Lenders, understandably against that backdrop, have stopped loosening their lending standards to corporate borrowers, according to the Fed’s Senior Loan Officer Survey."

-(Morgan Stanley) "is expecting chargeoffs to remain flat this year, but loan provisions to rise 30% as falling recoveries spell the end to the long improvement in credit quality."---Has the equity market priced in the expectation of increasing reserves?

-"Even a slight reduction in market liquidity will make it more difficult efficiently to lay off risk, so lending standards will likely tighten further."---That seems like a reasonable statement to me.

There is are a number of other points to chew on in Roubini's post; it's well worth a read.

Monday, February 26, 2007

Links of the day

Downey Financial: Underlying Fundamentals Continue to Deteriorate....Good analysis of an non-subprime lender's exposure to exotic mortgage loans

Friday, February 23, 2007

American Idol vs Grammys-2006

I was very amused when I saw this story posted on the website of a local TV station. 28.3 million people watched American Idol while only 15.1 million watched the Grammys as the two shows went head to head last year.

Part of the explanation for this result is tied to what New York Attorney General Eliot Spitzer was doing at the time.

According to the AP,

'Payola' investigation targets national radio conglomerates

Michael Gormley

Feb. 9, 2006 12:00 AM ALBANY, N.Y. - New York Attorney General Eliot Spitzer said Wednesday that he has subpoenaed nine of the nation's largest radio conglomerates in his "payola" investigation of major artists and songs. He claims they got airtime because of payoffs by recording companies.

"A lot of the major songs have been implicated in this and it showed how pervasive the payola infrastructure had become," Spitzer said. "Major artists, major songs were sent up the charts through improper payments to buy spins on the air that translated into sales."

The companies that have received subpoenas control thousands of stations nationwide, including Clear Channel Communications Inc., Infinity, which now operates as CBS Radio, Citadel Broadcasting Corp., Cox Radio Inc., Cumulus Broadcasting Inc., Pamal Broadcasting Ltd., Entercom Communications Corp., Emmis Communications Corp. and ABC Inc., according to court records filed by Spitzer.

Two major recording companies agreed last year to settle their parts of the investigation. Warner Music Group Corp. agreed last year to pay $5 million, and Sony BMG Music Entertainment agreed to pay $10 million.

Artists and writers are not targets, Spitzer's office said. In fact, they have supported the investigation and provided several complaints to assistant investigators.

"Cox Radio has cooperated fully with Attorney General Spitzer's investigation," said Bob Neil, president and chief executive of Cox.

Jason Finkelberg, general manager of Pamal Broadcasting, based in Beacon, N.Y., said he knows of no payola being practiced.

Spitzer has relied on civil laws in the payola case because the criminal laws are more specific and difficult to violate.

The radio probe involves Jennifer Lopez's I'm Real and John Mayer's song Daughters. Songs by other artists are also being examined.

Today, payola is in the form of direct bribes to radio programmers, including airfare, electronics, iPods and tickets.

-------------------------------------------------------------------

What this all means is that the songs that are playing on the top 40 are not up there because people like those songs, but are there because label execs are bribing the DJ's to play particular songs. That explains how REO Speedwagon became popular....

Part of the explanation for this result is tied to what New York Attorney General Eliot Spitzer was doing at the time.

According to the AP,

'Payola' investigation targets national radio conglomerates

Michael Gormley

Feb. 9, 2006 12:00 AM ALBANY, N.Y. - New York Attorney General Eliot Spitzer said Wednesday that he has subpoenaed nine of the nation's largest radio conglomerates in his "payola" investigation of major artists and songs. He claims they got airtime because of payoffs by recording companies.

"A lot of the major songs have been implicated in this and it showed how pervasive the payola infrastructure had become," Spitzer said. "Major artists, major songs were sent up the charts through improper payments to buy spins on the air that translated into sales."

The companies that have received subpoenas control thousands of stations nationwide, including Clear Channel Communications Inc., Infinity, which now operates as CBS Radio, Citadel Broadcasting Corp., Cox Radio Inc., Cumulus Broadcasting Inc., Pamal Broadcasting Ltd., Entercom Communications Corp., Emmis Communications Corp. and ABC Inc., according to court records filed by Spitzer.

Two major recording companies agreed last year to settle their parts of the investigation. Warner Music Group Corp. agreed last year to pay $5 million, and Sony BMG Music Entertainment agreed to pay $10 million.

Artists and writers are not targets, Spitzer's office said. In fact, they have supported the investigation and provided several complaints to assistant investigators.

"Cox Radio has cooperated fully with Attorney General Spitzer's investigation," said Bob Neil, president and chief executive of Cox.

Jason Finkelberg, general manager of Pamal Broadcasting, based in Beacon, N.Y., said he knows of no payola being practiced.

Spitzer has relied on civil laws in the payola case because the criminal laws are more specific and difficult to violate.

The radio probe involves Jennifer Lopez's I'm Real and John Mayer's song Daughters. Songs by other artists are also being examined.

Today, payola is in the form of direct bribes to radio programmers, including airfare, electronics, iPods and tickets.

-------------------------------------------------------------------

What this all means is that the songs that are playing on the top 40 are not up there because people like those songs, but are there because label execs are bribing the DJ's to play particular songs. That explains how REO Speedwagon became popular....

Milton Friedman on the Euro

is at this post.....the key point that he made was that this is the first currency recognized as official by independent states that is not backed by gold.

The quote:

The euro is going to be a big source of problems, not a source of help. The euro has no precedent. To the best of my knowledge, there has never been a monetary union, putting out a fiat currency, composed of independent states.

There have been unions based on gold or silver, but not on fiat money—money tempted to inflate—put out by politically independent entities...

The quote:

The euro is going to be a big source of problems, not a source of help. The euro has no precedent. To the best of my knowledge, there has never been a monetary union, putting out a fiat currency, composed of independent states.

There have been unions based on gold or silver, but not on fiat money—money tempted to inflate—put out by politically independent entities...

Links of the day

Hannibal and the Romans......

A UCLA Anthropologist's Study of Urban Land Use by Middle Class People in Los Angeles...this demands a detailed analysis but don't have the time now...absolutely outstanding information

Mish has an information-loaded post on the proportion of jobs linked to the housing industry in Florida: the prospects look grim for that state if a full-scale housing bust takes place there.

Incentive of oil producers and owners is now to hoard..Excellent explanation of why by Dr. Arnold Kling...hoarding is a positive feedback to increasing prices.

San Diego County pension fund...two good quotes are.... "financial instruments could be particularly problematic given a potential conflict between the incentives facing an individual pension fund manager and the best interests of the future retirees whose assets he or she is managing. If the manager can turn in well-above-market returns five years in a row, the manager is likely to be spectacularly rewarded over that period. Whether the beneficiaries are actually paid many years later down the road will be somebody else's problem...." and "When I heard about the disastrously irresponsible investments made by the Amaranth hedge fund, my first reaction was, who would be so stupid to have put up the margin requirements for such a scheme? The answer turned out to be found in my own backyard-- the San Diego County Employees Retirement Association apparently donated over a hundred million dollars to this worthy cause."

A UCLA Anthropologist's Study of Urban Land Use by Middle Class People in Los Angeles...this demands a detailed analysis but don't have the time now...absolutely outstanding information

Mish has an information-loaded post on the proportion of jobs linked to the housing industry in Florida: the prospects look grim for that state if a full-scale housing bust takes place there.

Incentive of oil producers and owners is now to hoard..Excellent explanation of why by Dr. Arnold Kling...hoarding is a positive feedback to increasing prices.

San Diego County pension fund...two good quotes are.... "financial instruments could be particularly problematic given a potential conflict between the incentives facing an individual pension fund manager and the best interests of the future retirees whose assets he or she is managing. If the manager can turn in well-above-market returns five years in a row, the manager is likely to be spectacularly rewarded over that period. Whether the beneficiaries are actually paid many years later down the road will be somebody else's problem...." and "When I heard about the disastrously irresponsible investments made by the Amaranth hedge fund, my first reaction was, who would be so stupid to have put up the margin requirements for such a scheme? The answer turned out to be found in my own backyard-- the San Diego County Employees Retirement Association apparently donated over a hundred million dollars to this worthy cause."

Much medical research a waste of money

due to flaws in the design and carrying out of the studies. The Bayesian Heresy pointed out a story in The Economist which documents the poor quality of medical studies and includes this mind-boggling paragraph:

"Unfortunately, many researchers looking for risk factors for diseases are not aware that they need to modify their statistics when they test multiple hypotheses. The consequence of that mistake, as John Ioannidis of the University of Ioannina School of Medicine, in Greece, explained to the meeting, is that a lot of observational health studies—those that go trawling through databases, rather than relying on controlled experiments—cannot be reproduced by other researchers. Previous work by Dr Ioannidis, on six highly cited observational studies, showed that conclusions from five of them were later refuted. In the new work he presented to the meeting, he looked systematically at the causes of bias in such research and confirmed that the results of observational studies are likely to be completely correct only 20% of the time. If such a study tests many hypotheses, the likelihood its conclusions are correct may drop as low as one in 1,000—and studies that appear to find larger effects are likely, in fact, simply to have more bias."

Observational studies result in valid findings only one-fifth of the time!! And the public is basing its health policy decision making on these studies, many of which get a lot of publicity in the main stream media!!Gross accounting trickery

See Sanyo's Legal Problems Are Bad News for Goldman...

According to a Bloomberg story on this subject "Goldman, the world's most profitable securities firm, Daiwa and Sumitomo Mitsui invested 300 billion yen ($2.5 billion) in Sanyo in January 2006 in return for management control. New York-based Goldman and Daiwa SMBC, each bought 125 billion yen of preferred stock that can be converted into a 24.5 percent stake in the company and sold to outside investors without Sanyo's consent starting March 14."

So Goldman was about to be able to start dumping shares in Sanyo...there is certain to be quite a tale behind the timing of this disclosure.

An interesting related fact included in the Bloomberg story is that "the company is seeking buyers for its chipmaking unit in a transaction that may raise more than 100 billion yen($826 million..my addition), two people familiar with the plan said on Feb. 2. The company was forced to stop operations at its chip factory in Niigata, central Japan, after an October 2004 earthquake. Operating losses in the chip unit mounted to 17.7 billion yen in the year to March 2005 and 35.1 billion yen the following year...." I haven't noticed before specific indications of economic loss to a company attributable to an earthquake.

"Sanyo Electric Co. announced today its accounting practices are being investigated by the Securities and Exchange Surveillance Committee, sending shares down a whopping 21% in Tokyo trading. Wall Street Journal says the news has serious implications for Goldman Sachs, which helped bail Sanyo out of its difficulties last year by purchasing more than a billion dollars worth of preferred shares....The charges, reported in the Asahi Shimbun this morning, state the company misrepresented its F2004 losses by as much as $1.1 billion.....Fukoku Capital Management analyst Tomokatsu Mori: "The company lacks management competence."

So it's not just US companies that are cooking their books..who would have thought? I'll bet the people from Goldman's due diligence team on that preferred stock purchase choked on their Wheaties this morning. Certainly the audit opinions that were rendered for the periods in question weren't worth the paper they were printed on.According to a Bloomberg story on this subject "Goldman, the world's most profitable securities firm, Daiwa and Sumitomo Mitsui invested 300 billion yen ($2.5 billion) in Sanyo in January 2006 in return for management control. New York-based Goldman and Daiwa SMBC, each bought 125 billion yen of preferred stock that can be converted into a 24.5 percent stake in the company and sold to outside investors without Sanyo's consent starting March 14."

So Goldman was about to be able to start dumping shares in Sanyo...there is certain to be quite a tale behind the timing of this disclosure.

An interesting related fact included in the Bloomberg story is that "the company is seeking buyers for its chipmaking unit in a transaction that may raise more than 100 billion yen($826 million..my addition), two people familiar with the plan said on Feb. 2. The company was forced to stop operations at its chip factory in Niigata, central Japan, after an October 2004 earthquake. Operating losses in the chip unit mounted to 17.7 billion yen in the year to March 2005 and 35.1 billion yen the following year...." I haven't noticed before specific indications of economic loss to a company attributable to an earthquake.

Thursday, February 22, 2007

Links of the day

Your Government Is Getting More Transparent. Why Not Take a Look?...referring to the USA, and detailing how easy it has become to gain access to federal budget information using the internet...

Unexpected consequence of home foreclosure

The Housing Bubble Blog links to a story pointing out that "“Homeowners should know that although debt can be forgiven, it’s never forgotten. When a short sale, deed-in-lieu agreement or foreclosure occurs and a residential lender loses money on a loan, the lender will most likely file the loss with the IRS, and the former homeowner may end up owing thousands of dollars in taxable income.”

Update: Michael Shedlock also has flagged this nasty surprise for homeowners who have to exit their home through a short sale: "One in five sales is a short sale. That is pretty staggering. It will be interesting to watch this trend develop. What is clear is that lenders do not want those homes back. Equally clear is there are likely to be some huge tax consequences for forgiveness of debt some time down the road."

“‘That’s probably where we see kind of the biggest surprise on the part of our clients,’ said Jackie Pearlman, senior tax research coordinator for H&R Block. ‘Not only are they not aware it existed but are very surprised to understand that it’s income. The concept is really alien to many people.’”

“‘We all know intuitively that if you borrow money you don’t have the income,’ said Bill Purdy, a Soquel-based attorney in Santa Cruz County who represents clients with home lending problems and foreclosures. ‘If you don’t have to pay it back, it can become income.’”

“But if the lender takes a loss selling a property, let’s say $100,000, the company will file with the IRS, and the client will receive a 1099-C for the amount.”

“Purdy said many people try to ignore the problem. ‘The problem is that people do nothing,’ he said. ‘They freeze like deer in headlights.’”

“But none of this matters to the IRS, which knows only that a 1099-C was distributed as taxable income. ‘They will assume it’s taxable until informed otherwise,’ he said. ‘And you don’t want to wait for that notice in the mail.’”

“Adarsh Sangani, director of residential lending for Fremont Bank, said his bank doesn’t issue many 1099-Cs to its customers. ‘Only if a customer doesn’t respond to collection calls, a letter and a collection agency,’ he said.”

I think what is being referred to here is even though the bank makes a short sale, the homeowner still had a paper profit based on their original purchase price on the home; that is what becomes potentially taxable income.Update: Michael Shedlock also has flagged this nasty surprise for homeowners who have to exit their home through a short sale: "One in five sales is a short sale. That is pretty staggering. It will be interesting to watch this trend develop. What is clear is that lenders do not want those homes back. Equally clear is there are likely to be some huge tax consequences for forgiveness of debt some time down the road."

Wednesday, February 21, 2007

Insight on the subject of stock buybacks vs dividends

Over at Mish's Global Economic Trend Analysis , he discusses the subject of how the ratio of CEO pay to the average worker pay is insanely higher in the US than in any other country. He quotes from a speech by an SEC commissioner to that effect as follows:

In 1982, the ratio between chief executives and the average employee was 42:1. In 2004, the ratio of the average CEO pay to that of the average non-management worker in the US was 431:1. There is certainly no evidence that today's executives in the U.S. are 10 times better than twenty years ago. The US ratio far exceeds any international comparison, which remain closer to the historical average. Although internationally there has been a trend towards increased "US-style" pay, according to a 2001 report by management consultants Towers Perrin the same ratio in other heavily developed nations was 25:1 in the case of the UK, 16:1 in France, 11:1 in Germany and as low as 10:1 in Japan (as compared to 531:1 in the US in that same year).

Mish's analysis of the cause of the disparity includes a discussion of how CEOs whose pay includes significant stock option grants have a strong incentive to return capital to shareholders through stock buybacks instead of dividends. Dividend payments now are worthless to the CEO who holds stock options that he/she cannot exercise until some time in the future. So the CEO will do share buybacks rather than dividends. Mish's succinct statement of this: "every dime paid out in dividends reduces the value of all outstanding options."

Good stuff...

In 1982, the ratio between chief executives and the average employee was 42:1. In 2004, the ratio of the average CEO pay to that of the average non-management worker in the US was 431:1. There is certainly no evidence that today's executives in the U.S. are 10 times better than twenty years ago. The US ratio far exceeds any international comparison, which remain closer to the historical average. Although internationally there has been a trend towards increased "US-style" pay, according to a 2001 report by management consultants Towers Perrin the same ratio in other heavily developed nations was 25:1 in the case of the UK, 16:1 in France, 11:1 in Germany and as low as 10:1 in Japan (as compared to 531:1 in the US in that same year).

Mish's analysis of the cause of the disparity includes a discussion of how CEOs whose pay includes significant stock option grants have a strong incentive to return capital to shareholders through stock buybacks instead of dividends. Dividend payments now are worthless to the CEO who holds stock options that he/she cannot exercise until some time in the future. So the CEO will do share buybacks rather than dividends. Mish's succinct statement of this: "every dime paid out in dividends reduces the value of all outstanding options."

Good stuff...

Key points in final 4th quarter US GDP report

Defense spending decreased 8.9%

Final 2005 GDP percentage change: 3.5% - that is a healthy number

Source: BEA

Final 2005 GDP percentage change: 3.5% - that is a healthy number

Source: BEA

Ford Hybrid Escape a success

A press release from Ford found on Yahoo: Ford Escape Hybrid Electric Vehicle on Track for All-Time Record Sales on Eve of Earth Day.

This is what American carmakers need to succeed: well designed vehicles. Get that right and Ford and GM will be just fine. GM's problem is that their design department hasn't got a clue.

This is what American carmakers need to succeed: well designed vehicles. Get that right and Ford and GM will be just fine. GM's problem is that their design department hasn't got a clue.

Changes at Sun Microsystems

I think that McNealy leaving is a good thing, as apparently he was the only one standing in the way of mass layoffs at Sun. The word is that he was keeping the extra programmers around as an investment in potential future software development. That's commendable but eventually any company has to have a level of employees that makes the profit and loss statement work.

I don't think that the ex-Sun employees have had much difficulty finding work.

I think that Sun is heading in the right direction with its business strategy; they just need to get their costs under control. Taking the AMD Opteron and developing systems based on it and pushing them hard has been and will continue to be extremely successful. Sun was one of the first OEM's to take AMD's product and run with it. This is going to be a long term win for Sun.

Sun's primary problem has been that they were so successful during the dot com boom that they weren't focusing on building future business but rather moving their servers out the door as fast as they could. It takes time to re-orient a large company in the face of wrenching changes like the dot com boom and bust. HP has taken plenty of lumps but they are on the road to success again as well.

I don't think that the ex-Sun employees have had much difficulty finding work.

I think that Sun is heading in the right direction with its business strategy; they just need to get their costs under control. Taking the AMD Opteron and developing systems based on it and pushing them hard has been and will continue to be extremely successful. Sun was one of the first OEM's to take AMD's product and run with it. This is going to be a long term win for Sun.

Sun's primary problem has been that they were so successful during the dot com boom that they weren't focusing on building future business but rather moving their servers out the door as fast as they could. It takes time to re-orient a large company in the face of wrenching changes like the dot com boom and bust. HP has taken plenty of lumps but they are on the road to success again as well.

Massive accounting fraud at Computer Associates...FACT

The point: this type of fraud doesn't occur without approval at the highest levels of a company. The story is at Yahoo News; here are a couple of excerpts.

---------------

"Sanjay Kumar, the former chief executive of CA Inc. (NYSE:CA - news), pleaded guilty on Monday to securities fraud, perjury and obstruction of justice charges related to his role a $2.2 billion accounting scheme at the computer software company."

---------------

"Kumar, who left Computer Associates International Inc., as it was known, in June 2004, improperly booked software license revenue from 1999 to 2000 in order to meet Wall Street analysts' quarterly earnings expectations and then lied to investigators about it, according to the indictment.

"As part of the scheme, Kumar and other sales executives back-dated software license contracts so that revenue would be recorded in a quarter where extra sales were needed to help the Islandia, New York, based company to meet or exceed Wall Street estimates, the indictment said.

---------------

"Sanjay Kumar, the former chief executive of CA Inc. (NYSE:CA - news), pleaded guilty on Monday to securities fraud, perjury and obstruction of justice charges related to his role a $2.2 billion accounting scheme at the computer software company."

---------------

"Kumar, who left Computer Associates International Inc., as it was known, in June 2004, improperly booked software license revenue from 1999 to 2000 in order to meet Wall Street analysts' quarterly earnings expectations and then lied to investigators about it, according to the indictment.

In one instance, prosecutors charged that Kumar paid off a customer who threatened to tell the government about a bogus software deal. The payoff of $3.7 million was made while Kumar knew an investigation was pending against the company."

------------"As part of the scheme, Kumar and other sales executives back-dated software license contracts so that revenue would be recorded in a quarter where extra sales were needed to help the Islandia, New York, based company to meet or exceed Wall Street estimates, the indictment said.

In one instance, Kumar flew in the company jet to Paris where he personally negotiated a license agreement for $32 million. That contract was backdated to make it appears that it had been finalized and signed on June 30, 1999, the government said."

Walmart demonstrates some leadership

From the Wall Street Journal via Daniel Gross(I have added bold highlights):

-----------------------------

Wal-Mart Stores Inc.'s effort to increase the efficiency of its trucking fleet -- a key part of the its plans to cut costs and portray itself as more environmentally friendly -- is running ahead of schedule.

Increased fuel efficiency is a worthwhile goal from the shareholders' perspective regardless of the PR benefits.

-----------------------------

Wal-Mart Stores Inc.'s effort to increase the efficiency of its trucking fleet -- a key part of the its plans to cut costs and portray itself as more environmentally friendly -- is running ahead of schedule.

In October, the Bentonville, Ark., retailer unveiled plans to make its trucking fleet 25% more fuel-efficient within three years. The fleet of 7,100 trucks already is on track to become 18% more efficient over the next year alone, said Johnnie Dobbs, Wal-Mart's executive vice president of logistics. "At this point, we feel pretty comfortable we can make the 25% goal," Mr. Dobbs said.

The high-throttle progress is a boost to Wal-Mart's recent efforts to curb its operating expenses amid soaring prices for energy and health care. Last fall in an interview with The Wall Street Journal, Chief Financial Officer Tom Schoewe singled out Wal-Mart's trucking fleet along with work-shift management as a top priority for reining in costs.

By increasing its trucks' fuel-efficiency by one mile a gallon from their recent average of 6.5 miles a gallon -- a 15% improvement -- Wal-Mart could add $50 million a year to its income, Mr. Schoewe said.

The effort comes as the price of fuel is again soaring. The Energy Department said this week the U.S. price of diesel fuel averaged $2.765 a gallon, more than 50 cents higher than the year before.

Mr. Dobbs said the bulk of the savings for Wal-Mart's trucking fleet thus far have come from the installation of auxiliary units that power the air conditioning when a truck is parked, eliminating the need to run the engine. Wal-Mart's trucks also are benefiting from wider tires that can carry bigger payloads, aerodynamic skirts and cowlings that cut wind resistance, and new additives that give diesel more bang for the buck.

Wal-Mart executives said they are surprised to be exceeding their near-term goals so early. The company also has set a longer-term goal to double the efficiency of its truck fleet in 10 years. While the early gains have come from "low-hanging fruit," meeting the 10-year target "will be the real stretch," as most of the energy savings are to come from technology that is still being developed, Mr. Dobbs said.

Future improvements may come from lighter truck designs, more efficient engines and transmissions, and hybrid technologies that use electricity and hydrogen power, Mr. Dobbs said. Researchers also are testing "biodiesel" manufactured from animal and vegetable oils, but "the jury is still out on that," Mr. Dobbs said.

The plans are a pillar of an environmental initiative that Wal-Mart announced with much fanfare in October. In addition to slashing transportation costs, the program also seeks to reduce greenhouse gases from existing stores and distribution centers by 20% over the next seven years.

As for new stores, Wal-Mart aims to introduce a design within four years that is at least 25% more energy-efficient. Those developments could also pay off, as the price of electricity and natural gas have soared along with the price of oil.

In addition to upgrading its truck fleet, Wal-Mart this year has purchased 100 hybrid cars for the company's market managers, who typically oversee eight to 15 stores each. "They tend to do a lot of driving in between stores, so that could be a real savings," Mr. Dobbs said.

------------------------------------------Increased fuel efficiency is a worthwhile goal from the shareholders' perspective regardless of the PR benefits.

Tuesday, February 20, 2007

Links of the day

Spanish bank buying Compass in $10B deal....from the Austin Business Journal...given the state of the lending environment in the US now, it will be interesting to see how this foreign direct investment turns out a few years down the road...

Japan: To Raise or not to Raise, That is the Question....referring to short-term interest rates, of course...

Blair to announce Iraq withdrawal plan....according to the linked Yahoo News article, Britain has 7,100 soldiers in Iraq currently. That is a puny number, compared to the total population of Great Britain of about 61 million people. That number of troops is approximately one one-thousandth of the UK population. According to icasualties.org, which has been keeping track of casualties in Iraq since the beginning of what the US calls Operation Iraqi Freedom, a total of 132 UK soldiers have lost their lives in Iraq during this time period.

Japan: To Raise or not to Raise, That is the Question....referring to short-term interest rates, of course...

Blair to announce Iraq withdrawal plan....according to the linked Yahoo News article, Britain has 7,100 soldiers in Iraq currently. That is a puny number, compared to the total population of Great Britain of about 61 million people. That number of troops is approximately one one-thousandth of the UK population. According to icasualties.org, which has been keeping track of casualties in Iraq since the beginning of what the US calls Operation Iraqi Freedom, a total of 132 UK soldiers have lost their lives in Iraq during this time period.

Prospects for a glut of steel production-retrospective

The American Iron and Steel Institute's site had a story from the Financial Times discussing this:

Steel Glut Unlikely, Expert Predicts

February 13, 2006

Financial Times

By PETER MARSH

Fears that overproduction in China will de-stabilise the global steel business in the coming year may be misplaced, according to industry experts.

The projections increase the chance that Mittal Steel, having launched an Euros 18.6bn (USDollars 22.1bn) takeover bid for rival steel company Arcelor, may be forced in the coming weeks to increase its cash-and-shares offer.

Mike Locker, president of Locker Associates, a US steel consultancy, said: "My view is that the steel business in 2006 will be steady and flat. I think the Chinese government will act to ensure that the risk of overproduction by Chinese mills will be relatively small."

Some worries have been expressed in the past year that output overruns in China - responsible for nearly a third of world steel production - could lead to the country becoming a large net exporter of steel. The extra material entering global markets could depress prices and damage steel industry profitability.

However, forecasts by Meps, a UK steel consultancy, suggest that net exports by China of steel in 2006 will be only 7m tonnes, compared with 0.5m tonnes in 2005. In 2004, China was a net importer of steel of 12.8m tonnes, with imports of 33.2m tonnes and exports of 20.4m tonnes.

Peter Fish, managing director of Meps, said : "The picture for 2006 that we are seeing for the steel industry is rather benign and not particular exciting, but this is positive from the point of view of the steel industry which is not helped by large swings in prices and supply-and-demand conditions."

Luxembourg-based Arcelor is fighting the unsolicited offer by Mittal, headed by Indian billionaire Lakshmi Mittal, on the grounds that the bid both undervalues Arcelor and does not follow industrial logic.

Perceptions that the steel business is entering a fairly calm period, with relatively few risks of a sudden fall in prices, may help to maintain investors' thinking that the current high valuations for steel companies globally are justified by fundamental economics.

Some steel industry onlookers believe Mittal might need to raise its bid - or increase the amount of cash in the offer - to improve its chance of winning over Arcelor shareholders. Mr Mittal has said Mittal has no plans to increase its bid.

This week both companies are announcing their financial results for 2005. On Wednesday Mittal, created in its current form from a previous merger only one year ago, is expected by analysts to announce pre-tax profits of some Dollars 4.6bn on sales of Dollars 28.8bn.

The following day Arcelor is thought likely to announce pre-tax profits of Euros 4.3bn, up from Euros 3bn in 2004, on sales of Euros 32.3bn.

According to projections by Meps, average world steel prices will fall only marginally from Dollars 549 a tonne to Dollars 542 a tonne by January 2007.

---------------------------------------------

Here are the actual prices for 2006 courtesy of MEPS:

Steel Glut Unlikely, Expert Predicts

February 13, 2006

Financial Times

By PETER MARSH

Fears that overproduction in China will de-stabilise the global steel business in the coming year may be misplaced, according to industry experts.

The projections increase the chance that Mittal Steel, having launched an Euros 18.6bn (USDollars 22.1bn) takeover bid for rival steel company Arcelor, may be forced in the coming weeks to increase its cash-and-shares offer.

Mike Locker, president of Locker Associates, a US steel consultancy, said: "My view is that the steel business in 2006 will be steady and flat. I think the Chinese government will act to ensure that the risk of overproduction by Chinese mills will be relatively small."

Some worries have been expressed in the past year that output overruns in China - responsible for nearly a third of world steel production - could lead to the country becoming a large net exporter of steel. The extra material entering global markets could depress prices and damage steel industry profitability.

However, forecasts by Meps, a UK steel consultancy, suggest that net exports by China of steel in 2006 will be only 7m tonnes, compared with 0.5m tonnes in 2005. In 2004, China was a net importer of steel of 12.8m tonnes, with imports of 33.2m tonnes and exports of 20.4m tonnes.

Peter Fish, managing director of Meps, said : "The picture for 2006 that we are seeing for the steel industry is rather benign and not particular exciting, but this is positive from the point of view of the steel industry which is not helped by large swings in prices and supply-and-demand conditions."

Luxembourg-based Arcelor is fighting the unsolicited offer by Mittal, headed by Indian billionaire Lakshmi Mittal, on the grounds that the bid both undervalues Arcelor and does not follow industrial logic.

Perceptions that the steel business is entering a fairly calm period, with relatively few risks of a sudden fall in prices, may help to maintain investors' thinking that the current high valuations for steel companies globally are justified by fundamental economics.

Some steel industry onlookers believe Mittal might need to raise its bid - or increase the amount of cash in the offer - to improve its chance of winning over Arcelor shareholders. Mr Mittal has said Mittal has no plans to increase its bid.

This week both companies are announcing their financial results for 2005. On Wednesday Mittal, created in its current form from a previous merger only one year ago, is expected by analysts to announce pre-tax profits of some Dollars 4.6bn on sales of Dollars 28.8bn.

The following day Arcelor is thought likely to announce pre-tax profits of Euros 4.3bn, up from Euros 3bn in 2004, on sales of Euros 32.3bn.

According to projections by Meps, average world steel prices will fall only marginally from Dollars 549 a tonne to Dollars 542 a tonne by January 2007.

---------------------------------------------

Here are the actual prices for 2006 courtesy of MEPS:

World Steel Prices US $/tonne | Steel Coil | Rolled Steel Plate | Rolled Steel Coil | Rod | Sections |

| Jan 2006 | 510 | 649 | 613 | 446 | 602 |

| Feb 2006 | 503 | 646 | 607 | 447 | 602 |

| Mar 2006 | 516 | 651 | 620 | 462 | 612 |

| Apr 2006 | 538 | 670 | 636 | 480 | 631 |

| May 2006 | 569 | 717 | 668 | 495 | 666 |

| Jun 2006 | 599 | 741 | 703 | 513 | 685 |

| Jul 2006 | 597 | 736 | 702 | 517 | 703 |

| Aug 2006 | 599 | 737 | 704 | 519 | 705 |

| Sep 2006 | 591 | 755 | 691 | 521 | 716 |

| Oct 2006 | 569 | 740 | 664 | 507 | 701 |

| Nov 2006 | 560 | 743 | 658 | 501 | 718 |

The Pentagon has no idea how much it spends

See the post titled The Pentagon's Broken Book-keeping at Defense Industry Daily which explains in some detail and points to further info...a must read for anyone interested in how the US government spends its money.

Mish's "Spotlight on Japan" a must read

His recent post titled "Spotlight on Japan" is loaded with hard data, snippets from the media regarding Japan's economy, and his own insights regarding Japan's situation (most of which I agree with.

Mish begins by posing the question "is Japan a nation of savers?" He says no, and gives some facts to back up that assertion. These facts include: that Japan has the highest ratio of national debt to gdp of any country by far; that Japan's national debt is the equivalent of $7 trillion US dollars now; and that the Japanese government doesnt think it will be able to balance its budget until after 2010.

There is a quote included from a prominent economist to the effect that Japan is still the world's single biggest creditor nation. Granted, Japan still holds a lot of US treasury debt but has maintained its government budgets by issuing skyrocketing amounts of its own debt. So they have become a debtor nation. Hence the issue that Mish discusses where if the Ministry of Finance raises interest rates that will drive foreign holders of Japanese debt to sell, driving interest rates up further and potentially choking off gdp growth. Japan should have paid for its government spending by selling the US securities but of course that would have driven up the price of the yen thus hurting exports.

In my view, the Japanese government needs to spend less and save more; and the average Japanese citizen needs to spend more and save less. Domestic consumption needs to be a greater proportion of Japan's GDP than it is now. Of course, that will be hard to accomplish with a rapidly shrinking population.

Mish begins by posing the question "is Japan a nation of savers?" He says no, and gives some facts to back up that assertion. These facts include: that Japan has the highest ratio of national debt to gdp of any country by far; that Japan's national debt is the equivalent of $7 trillion US dollars now; and that the Japanese government doesnt think it will be able to balance its budget until after 2010.

There is a quote included from a prominent economist to the effect that Japan is still the world's single biggest creditor nation. Granted, Japan still holds a lot of US treasury debt but has maintained its government budgets by issuing skyrocketing amounts of its own debt. So they have become a debtor nation. Hence the issue that Mish discusses where if the Ministry of Finance raises interest rates that will drive foreign holders of Japanese debt to sell, driving interest rates up further and potentially choking off gdp growth. Japan should have paid for its government spending by selling the US securities but of course that would have driven up the price of the yen thus hurting exports.

In my view, the Japanese government needs to spend less and save more; and the average Japanese citizen needs to spend more and save less. Domestic consumption needs to be a greater proportion of Japan's GDP than it is now. Of course, that will be hard to accomplish with a rapidly shrinking population.

The fundamental problem in health care economics

Thanks to "Econlog", I found this excellent quote:

"Citizens everywhere desire unrestricted access to state-of-the-art technologies. Increasingly, they insist on choice and control, too. Yet they are unwilling to pay what those things cost. People demand as a right the best health care money can buy, delivered in the way that best suits them, expense be damned. All that, and the price must be affordable.

Nowhere can this self-contradictory demand be satisfied."

Exactly...

"Citizens everywhere desire unrestricted access to state-of-the-art technologies. Increasingly, they insist on choice and control, too. Yet they are unwilling to pay what those things cost. People demand as a right the best health care money can buy, delivered in the way that best suits them, expense be damned. All that, and the price must be affordable.

Nowhere can this self-contradictory demand be satisfied."

Exactly...

More on Japan's demographic crisis

Alpha-Sources has a good discussion of the subject here...the primary idea being that just getting Japanese workers to work until they are much older than traditional retirement age is not going to be enough to generate enough GDP to pay the country's bills.

The fact that the country's total population is beginning to shrink means that shrinkage of GDP is almost inevitable...as Japan cannot continue to increase its exports indefinitely. At some point increased domestic consumption is necessary to generate GDP growth and that is difficult with a shrinking population.

The fact that the country's total population is beginning to shrink means that shrinkage of GDP is almost inevitable...as Japan cannot continue to increase its exports indefinitely. At some point increased domestic consumption is necessary to generate GDP growth and that is difficult with a shrinking population.

Google's technologies makes most sense inside an enterprise

This is due to the fact that within an enterprise the page rank algorithm that Google search is based on would be less vulnerable to spoofing and disruptive search engine optimization. Links between pages within the enterprise that are not legitimate or serve only to puff up an individual's particular contributions will be able to be quickly spotted and purged, and offenders can be disciplined.

Also, the various apps that Google has rolled out to the public would make a compelling package for an enterprise if packaged within a Google hardware appliance. I would see the package as follows:

-intranet search (i.e. Google's standard search functionality)

-alerts--employees receive alerts when content is posted to their company intranet

-blogger--employees can use a blog as a method of communicating to co-workers vs email

-calendar, docs, and spreadsheets--obvious replacement for Microsoft products

-gmail as in-house mail server--obvious replacement for Exchange

-wiki-Google will do something with the JotSpot technology they've got--obvious replacement for Notes and Sharepoint

-etc....

Also, the various apps that Google has rolled out to the public would make a compelling package for an enterprise if packaged within a Google hardware appliance. I would see the package as follows:

-intranet search (i.e. Google's standard search functionality)

-alerts--employees receive alerts when content is posted to their company intranet

-blogger--employees can use a blog as a method of communicating to co-workers vs email

-calendar, docs, and spreadsheets--obvious replacement for Microsoft products

-gmail as in-house mail server--obvious replacement for Exchange

-wiki-Google will do something with the JotSpot technology they've got--obvious replacement for Notes and Sharepoint

-etc....

Monday, February 19, 2007

Germany's efforts to solve its demographic problem

Over at Demography Matters, there is a thought-provoking post titled "Germany gives the family a try." Essentially the German government is considering various incentives for couples to have more children, or any children at all. The problem that I see is that the reason Germans are not having enough children to replace the elderly dying off is due to strongly held beliefs about family size that are not going to be swayed by a few government programs.

Links of the day

Entrepreneurs are Heroes....couldn't agree more.

MONEY QUESTIONS (AGAIN)....M2 appears to be increasing faster than the US economy..should we fear inflation?

Iran says insurgent bombers are trained in Pakistan...boo hoo...

Investors in mortgage-backed securities fail to react to market plunge....thanks to Calculated Risk for the link..a worthwhile discussion of the issues

MONEY QUESTIONS (AGAIN)....M2 appears to be increasing faster than the US economy..should we fear inflation?

Iran says insurgent bombers are trained in Pakistan...boo hoo...

Investors in mortgage-backed securities fail to react to market plunge....thanks to Calculated Risk for the link..a worthwhile discussion of the issues

Natural gas prices: some perspective

Here is are some charts that shows spot prices for oil and gas prices over the past year. The chart for natural gas shows a huge spike from August 2005 through the first of the year and then an equally huge dropoff.

Food for thought...

Longer term trends in natural gas prices-USA

See this chart from the US Energy Information Administration:

What strikes me in looking at this chart is how much more volatile the residential price has been. Utility companies providing natural gas to residential customers ought to be able to negotiate the same types of long term contracts as the other three categories of users.

I think I might find time to look at what my local public service commission has been allowing the gas company to do. Based on this information and the chart in my previous post, my gas bill ought to be going down.

Heretical analysis of US national debt

Over at The Skeptical Optimist, the US national debt is analyzed as if it were a perpetuity. The implication: that the principal will never have to be repaid and thus US taxpayers shouldn't worry about the size of the national debt or whether we're shortchanging our descendants. I wonder if policy makers at the Bank of Japan or the People's Bank of China have looked at their holdings of US Treasuries in this fashion? Somehow, I think that the Bank of Japan is going to want to unload those Treasuries at some point, or will at least stop buying new ones. For the issuer of a debt to be able to roll over that debt, the issuer needs to find a buyer willing to buy the new debt.

Dell's business model not so direct anymore

A press release by Dell summarized and annotated:

"Dell announced a four-year agreement to provide Unilever, one of the world's largest consumer products companies, with products and services worth about $40 million. The agreement provides for deployment and managed services for about 10,000 systems in the United States, Canada and Puerto Rico. Deployment is under way in the U.S. and is expected to be completed within the next few weeks. -Unilever didn't just dial Dell's 1-800 number and sign up for this deal; there had to have been plenty of face to face meetings to complete the deal. This does not fit into a "direct" sales model.

Dell is supplying Unilever with OptiPlex(TM) desktop and Latitude(TM) notebook computers along with deployment services to help ensure a smooth upgrade of its networked systems to predominantly industry-standard Dell hardware running Microsoft Windows XP software.

In addition to factory installing nearly 500 software applications for Unilever in the U.S., Dell is responsible for installation and data transfer services as well as managed services such as service desk, moves, adds, changes, desk-side support, software distribution and asset tracking. -These are relatively labor intensive services that don't fit into a low-inventory, high sales turnover business model.

Dell is also providing Unilever with asset recovery services to help recover outdated systems and prepare them for responsible recycling or donation."

"Dell announced a four-year agreement to provide Unilever, one of the world's largest consumer products companies, with products and services worth about $40 million. The agreement provides for deployment and managed services for about 10,000 systems in the United States, Canada and Puerto Rico. Deployment is under way in the U.S. and is expected to be completed within the next few weeks. -Unilever didn't just dial Dell's 1-800 number and sign up for this deal; there had to have been plenty of face to face meetings to complete the deal. This does not fit into a "direct" sales model.

Dell is supplying Unilever with OptiPlex(TM) desktop and Latitude(TM) notebook computers along with deployment services to help ensure a smooth upgrade of its networked systems to predominantly industry-standard Dell hardware running Microsoft Windows XP software.

In addition to factory installing nearly 500 software applications for Unilever in the U.S., Dell is responsible for installation and data transfer services as well as managed services such as service desk, moves, adds, changes, desk-side support, software distribution and asset tracking. -These are relatively labor intensive services that don't fit into a low-inventory, high sales turnover business model.

Dell is also providing Unilever with asset recovery services to help recover outdated systems and prepare them for responsible recycling or donation."

Friday, February 16, 2007

Labor force participation

Economist's View recently flagged a San Francisco Fed analysis of unemployment rates here.

Some key points:

-labor force participation was at a historical high in 2000.

-"Labor force participation rates are highest for those aged 25-54; after age 55, labor force participation rates fall continuously as individuals retire. Thus, the aggregate U.S. labor force participation rate is expected to fall as the baby boom generation ages and retires."

-"Participation rates of men 25-54 have been gradually falling for more than 40 years." I see this as a result of the entrance of women into the workforce. I think there are a significant number of men in this age range either living with their parents or living off their wives' pay.

Some key points:

-labor force participation was at a historical high in 2000.

-"Labor force participation rates are highest for those aged 25-54; after age 55, labor force participation rates fall continuously as individuals retire. Thus, the aggregate U.S. labor force participation rate is expected to fall as the baby boom generation ages and retires."

-"Participation rates of men 25-54 have been gradually falling for more than 40 years." I see this as a result of the entrance of women into the workforce. I think there are a significant number of men in this age range either living with their parents or living off their wives' pay.

Financial distress of the city of New Orleans

The New Orleans Times-Picayune has a story detailing a finance package the city has put together to keep the city running for a couple of years until the city recovers enough to pay its bills through tax revenue. Some key points:

-The city's tax revenue is projected to shrink from "$151 million in 2004 to $69 million in 2006. Officials also are projecting huge declines in revenue from property taxes, sanitation service fees and parking meter fines."

-"the city is expected to spend more on basic services than it takes in through tax revenue for each of the next five years, with deficits expected to total $618 million by the end of 2010."

-the city's optimistic forecast projects that its population will recover to 320,000 in three years. The article quotes an outside study forecasting that the city won't reach a population level of "272,000 residents, or slightly more than half its pre-Katrina population" until 2008.

These facts hammer home how grim New Orleans' situation is. If the city raises taxes down the road to help pay off the debts it is going to incur, that will likely drive away residents and business. If the city cuts back on services to reduce the cash burn, that too is likely to drive away residents and businesses. The city may never fully recover from the damage of Katrina.

-The city's tax revenue is projected to shrink from "$151 million in 2004 to $69 million in 2006. Officials also are projecting huge declines in revenue from property taxes, sanitation service fees and parking meter fines."

-"the city is expected to spend more on basic services than it takes in through tax revenue for each of the next five years, with deficits expected to total $618 million by the end of 2010."

-the city's optimistic forecast projects that its population will recover to 320,000 in three years. The article quotes an outside study forecasting that the city won't reach a population level of "272,000 residents, or slightly more than half its pre-Katrina population" until 2008.

These facts hammer home how grim New Orleans' situation is. If the city raises taxes down the road to help pay off the debts it is going to incur, that will likely drive away residents and business. If the city cuts back on services to reduce the cash burn, that too is likely to drive away residents and businesses. The city may never fully recover from the damage of Katrina.

Source of market risk under the radar

Daily II has a post Banks Succeed In Slashing Unconfirmed-Trade Backlog which discusses an improvement in the processing of credit derivative trades. The key in this story, though, is the result pointed out in the story that "the number of unconfirmed trades dropping 50% from 150,000 to 74,000 in the six months ending March 31."

So there were 74,000 trades executed that hadn't cleared on March 31; what if there were a market shock on that date? I don't know how the uncleared trades would be handled in the event of a major market move, but I think it likely that there would be a tremendous mess that would take significant amounts of time and expense to sort out. Plus, there would likely be significant losses to some firms that had made trades that were uncleared and turned out to be rejected.

The same story has this fun fact: "According to the FSA, it took the largest banks 44 days to confirm a basic credit derivatives trade and about twice that for complex deals." Anyone with an E-Trade account can get confirmation of a stock trade in a few seconds, by contrast.

So, credit derivatives are skyrocketing in their importance in global financial markets, have been noted as a relatively poorly understood potential source of systemic risk by world financial leaders (such as Greenspan), and yet the systems used to handle these securities are essentially a steaming pile of horse manure. Great!

So there were 74,000 trades executed that hadn't cleared on March 31; what if there were a market shock on that date? I don't know how the uncleared trades would be handled in the event of a major market move, but I think it likely that there would be a tremendous mess that would take significant amounts of time and expense to sort out. Plus, there would likely be significant losses to some firms that had made trades that were uncleared and turned out to be rejected.

The same story has this fun fact: "According to the FSA, it took the largest banks 44 days to confirm a basic credit derivatives trade and about twice that for complex deals." Anyone with an E-Trade account can get confirmation of a stock trade in a few seconds, by contrast.

So, credit derivatives are skyrocketing in their importance in global financial markets, have been noted as a relatively poorly understood potential source of systemic risk by world financial leaders (such as Greenspan), and yet the systems used to handle these securities are essentially a steaming pile of horse manure. Great!

Good post on JK Galbraith and the error of his thinking

is titled Technological change and the Almighty Corporation. The gist..advertising isn't all that effective.

Holy smokes!

Charles Hugh Smith's weblog today talks about hedge funds and who actually gets the profits from their activities. There is one mind-blowing statistic that he offers up:

Here is the top 10 hedge fund managers' income: The full top 10 list of hedge fund earners according to Trader Monthly includes:

1. T. Boone Pickens - estimated 2005 earnings $1.5bn +

2. Steven A. Cohen, SAC Capital Advisers - $1bn +

3. James H. Simons, Renaissance Technologies Corp. - $900m - $1bn

4. Paul Tudor Jones, Tudor Investment Corp. - $800m - $900m

5. Stephen Feinberg, Cerberus Capital Management - $500 - $600m

6. Bruce Kovner, Caxton Associates - $500m - $600m

7. Eddie Lampert, ESL Investments - $500m - $600m

8. David Shaw, D.E. Shaw & Co - $400m - $500m

9. Jeffrey Gendell, Tontine Partners - $300m - $400m

10. Louis Bacon, Moore Capital Management - $300m - $350m

10. Stephen Mandel, Lone Pine Capital - $300m - $350m

I thought it was pretty crazy when the White House released Vice President Cheney's tax return a few years ago and his adjusted gross income was $36 million!

Here is the top 10 hedge fund managers' income: The full top 10 list of hedge fund earners according to Trader Monthly includes:

1. T. Boone Pickens - estimated 2005 earnings $1.5bn +

2. Steven A. Cohen, SAC Capital Advisers - $1bn +

3. James H. Simons, Renaissance Technologies Corp. - $900m - $1bn

4. Paul Tudor Jones, Tudor Investment Corp. - $800m - $900m

5. Stephen Feinberg, Cerberus Capital Management - $500 - $600m

6. Bruce Kovner, Caxton Associates - $500m - $600m

7. Eddie Lampert, ESL Investments - $500m - $600m

8. David Shaw, D.E. Shaw & Co - $400m - $500m

9. Jeffrey Gendell, Tontine Partners - $300m - $400m

10. Louis Bacon, Moore Capital Management - $300m - $350m

10. Stephen Mandel, Lone Pine Capital - $300m - $350m

I thought it was pretty crazy when the White House released Vice President Cheney's tax return a few years ago and his adjusted gross income was $36 million!

Links of the day

Antarctic temperatures disagree with climate model predictions...the more hard data that can be gathered the better.

Why businesses fail

A worthwhile analysis of the subject from computerwire.com :

Business failure is an opportunity for new CEOs to build fortunes and reputations. But with failure now happening at Internet speed, it is time to learn the lessons of history. Tom Hughes reports.

When in mid-September 2000, the owner of the domain name and Web site F****dCompany.com (our asterisks) put it up for sale on auction site eBay, there were amazed reactions when bidding for the site reached $10 million.

The reactions were short lived. A day later the auction was revealed as a practical joke. Yet, in terms of Web metrics, the site is probably worth the money. It also has a dedicated user base that competes to pick dot-com failures and is awarded points for predicting disasters, from minor public relations errors, to buyouts and bankruptcies.

In the process, the company may have revealed the investment community in a harsh and unforgiving light, but the true value of F****dCompany is that it shows how businesses are collapsing for the same reasons they always have, but are failing faster than ever before.

In IT more than any other market, the beneficiary of an ailing business is often the manager who is parachuted in to turn around the company's fortunes. One such man is CEO of IBM Lou Gerstner, who is said to have reversed Big Blue's decline during his seven-year stewardship. For this, Gerstner received a $21 million signing bonus, has share options worth $90 million, and was paid a salary of $9 million in 1999. Many investors and disaffected IBM watchers, however, argue that IBM's turnaround is merely the result of cost-cutting and financial engineering - a very 1980s benchmark of management success.

A more timely example is turnaround king Charles Wang, chairman and ex-CEO of mainframe software company Computer Associates. In mid-1998, CA's board approved Wang a $655 million issue of stock if the share price of the company doubled. It did, although Wang (along with two other executives) was forced to pay back a quarter of the award in March this year.

Ironically, Wang's success was in founding and shaping a multi-billion dollar entity that preyed on failing software companies. But even he is not immune to failure. CA rushed out a profit warning on 4 July 2000 (Independence Day and a national holiday). Shares were hit hard the day after, falling 42.6% from $51.33 to $29.44. As a result Wang resigned, and took up the post of chairman, to be replaced by COO Sanjay Kumar.

The reason for the collapse was two-fold. CA had done something that the financial community dislikes: rushing information past it during a national holiday. But the profit warning, which noted falling sales of mainframe software, also suggested that CA's core business was failing faster than Wall Street expected, and called into the question the rationale behind its recent $8 billion acquisitions.

Kumar's CA now plans to sell off or list either its growth or non-core businesses, many of which - such as Sterling Software's Federal Systems business - it acquired just six months before. But the fact remains that the world's number three software company's September market capitalisation of $14.6 billion was roughly that of a hot start-up with a reasonable financial history.

Reasons for failure

For many managers, the idea of turning around an ailing company is seductive: they get the kudos of the company's reversal of fortune, and share options at a depressed price. But why do many companies fail?

Pat Martin is the new CEO of enterprise storage vendor Storage Technology (StorageTek), which has been in effective decline for years because of its inability to create significant growth outside its original high-end tape archive business.

Martin identifies the company's error: signing an exclusive three-year deal with IBM in 1996 to distribute its Iceberg RAID (redundant array of inexpensive disk) devices. But IBM - which was filling a hole in its portfolio - walked away from the agreement, launched competing products, and won a number of StorageTek accounts. The end of the agreement has hit StorageTek hard: this year its revenue will fall from $2.4 billion in 1999 to around $2.0 billion, mainly because of the shortfall into the Big Blue yonder.

Martin's solution is deceptively simple: "We have to grow," he says, echoing the familiar cry of any ailing corporation entertaining potential investors.

But far more interesting than StorageTek's insubstantial strategy, was its route to failure: it educated the market about a new technology, then failed to deliver it. In the process, it handed a $3 billion-a-year opportunity to EMC - which until the early 1990s was an unknown circuit board assembler.

Network attached storage pioneer Auspex Systems has similarly lost its way, admits new president Michael Worhach. The company made a bet on Windows NT in 1998 with its new low-end product line, only to see little demand in the market. At the same time, the engineering team lost focus on its core enterprise Unix products and, as a result, the company hit serious financial difficulties.

Auspex has now called in turnaround specialist Regent Pacific, which plans to put the vendor - whose competitor, Network Appliance, is increasing its revenue at 120% per quarter - back on track within a year.

Pleasing Wall Street?

"Nasdaq forces CEOs to be dishonest," claims Dr Zvi Marom, CEO of Israeli networking equipment manufacturer BATM Advanced Technologies. The reason is simple: companies' values are based on discounted cash flow models. This is the total earnings (as a measure of cashflow) that a company will generate over 20 years (normally), discounted for a return equivalent to base interest rates and a further reduction in the long-term risk.

So when a company experiences lower than expected growth, reports late, or indicates other underlying problems, its share price can take an unexpectedly large hit. And when it does more than one of these things - as CA did in July 2000 - the punishment is severe.

But the worst mistake in this area - which is often repeated in the IT industry - is to be caught cheating, as the share price collapse of mainframe tools company Compuware indicated after its own profit warning. The company had been riding a wave of acquisitions, but falsely booked future service revenue into its profit and loss account.